UK cities: Where to invest

With property sectors experiencing varied success in investment terms, Stacey Meadwell finds out how the top six cities are performing and explores rents and yields across the markets

With property sectors experiencing varied success in investment terms, Stacey Meadwell finds out how the top six cities are performing and explores rents and yields across the markets

Office data

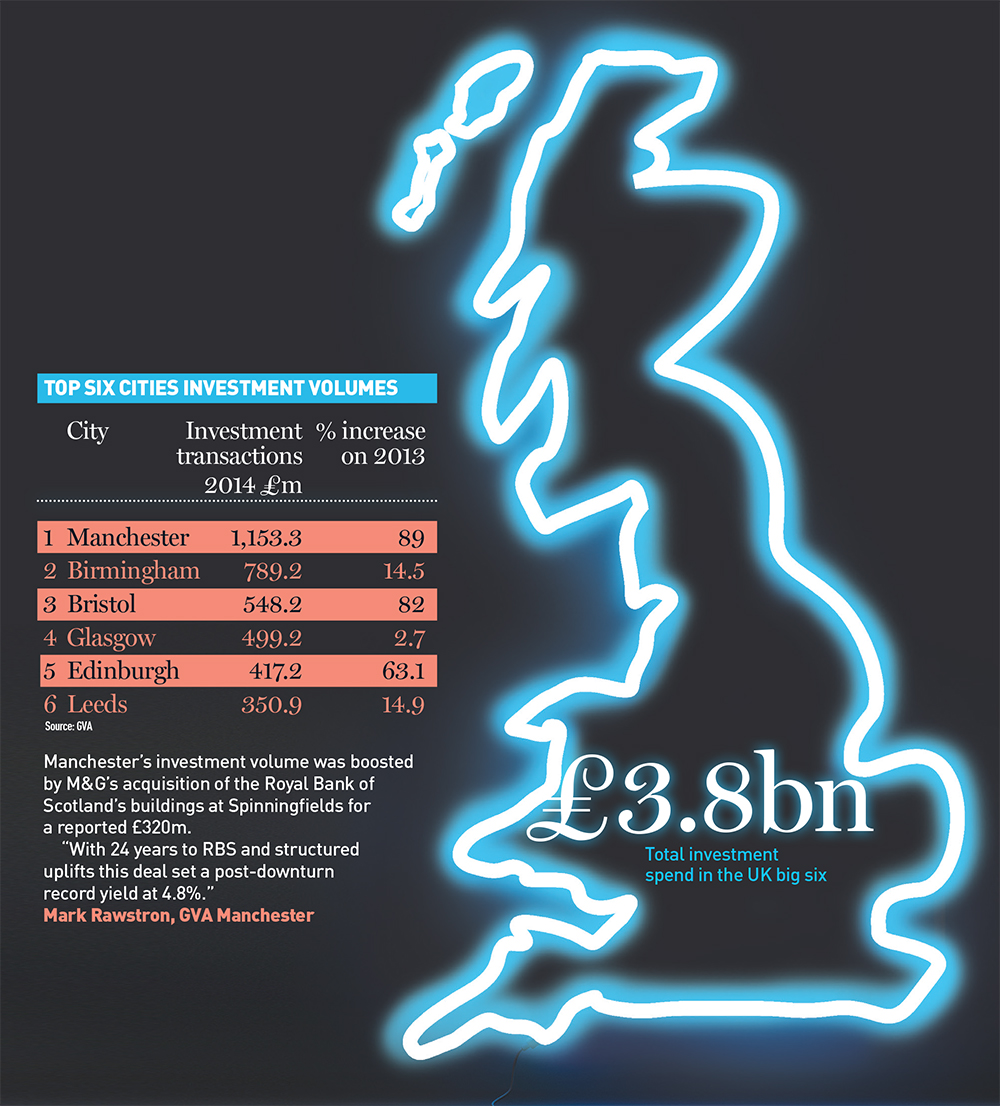

Last year was a bumper one for the office market across the UK’s six biggest cities, writes Stacey Meadwell. All have seen rents rise and investment yields compress. Manchester and Edinburgh command the highest rents, with the northern capital experiencing the highest take-up of space last year.

Speculative development has re-emerged. Manchester and Leeds have the most space under construction reflecting developer confidence in the recovering market. In Manchester schemes such as 2 St Peter’s Square are under way. Bristol was one of the first cities to see speculative development, with two schemes, Queen Square and Glass Wharf, due to complete this year – but both have secured at least partial prelets.

With demand continuing to rise and a historic lack of development during the economic downturn, a shortage of supply remains a concern. According to GVA, Birmingham has the least amount of stock available with 1.2 years of supply based on take-up trends.

This, of course, could have a continuing positive impact on rents as occupier appetite for new office space in the key cities continues to grow.

Retail data

It wasn’t so long ago that news headlines were full of empty shops and administrations, writes Stacey Meadwell, and while the retail market remains challenged by online shopping there are a number of developments under way which underpin confidence in the sector longer term. The Victoria Gate in Leeds is one example, and Scotland’s two biggest shopping centres could both see major extensions start construction this year.

Industrial data

The UK’s industrial market has, arguably, been a little slower to recover from the recession than the office market but there are certainly positive signals coming from market data. Demand is rising and supply shortages mean that speculative development may become a little more prevalent.

{kind=link}