As overworked agents headed off on their summer holidays after a bumper first half of the year, the London office market seemed, on the face of things, to have settled down for a quieter third quarter. Take-up fell more than 20% on Q3 2014, while there were only two deals of more than 100,000 sq ft.

But dig a little deeper and the figures show a market still moving at a bustling pace – but with very real constraints on supply – and most agents, rather than sounding rested after a couple of weeks off, reported a hectic three months.

Overall picture

Rental growth underpins investment

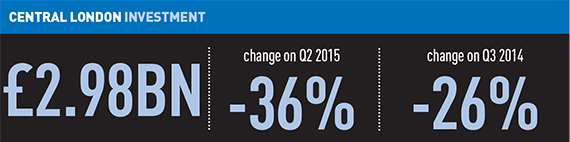

Wobbles in the Chinese market have failed to seriously dent investment into London offices. Though headline investment was slightly down on last year, rental growth continues to be a draw.

“Both overseas and domestic buyers are focused on assets that will perform best as rent increases come through,” says Knight Frank’s Nick Braybroook. “People are very keen to get their hands on development opportunities: multi-let assets or assets with low rent passing and rent reviews coming up. If anything, it’s the longer, drier income that is harder to find a home for.

“ There is always somebody who feels that the market has an advantage for them. There’s more caution in the market, but the fundamentals on the occupational side are so strong they will win the day.”

Start your free trial today

Your trusted daily source of commercial real estate news and analysis. Register now for unlimited digital access throughout April.

Including:

Breaking news, interviews and market updates

Expert legal commentary, market trends and case law

In-depth reports and data-led analysis

As overworked agents headed off on their summer holidays after a bumper first half of the year, the London office market seemed, on the face of things, to have settled down for a quieter third quarter. Take-up fell more than 20% on Q3 2014, while there were only two deals of more than 100,000 sq ft.

But dig a little deeper and the figures show a market still moving at a bustling pace – but with very real constraints on supply – and most agents, rather than sounding rested after a couple of weeks off, reported a hectic three months.

Overall picture

While take-up was down, deal numbers rose 32% on the same period last year, and were only 2% down on Q2. Indeed, the 438 deals were the highest number yet that EGi has recorded in a third quarter .

“It did not feel like August,” says Phillip Pearce, central London executive director at Savills, “it felt pretty robust, to be honest. If anything you have to question how sustainable is that trend.”

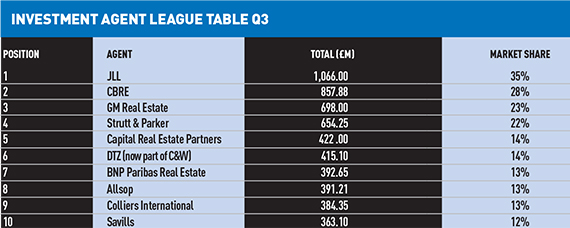

An absence of big ticket disposals put a dent in the totals of the big players – though it failed to dislodge JLL and CBRE from first and second place – but the plethora of smaller deals allowed fresh blood into the top 10. City fringe specialists Hatton Real Estate and West End and Midtown players Edward Charles & Partners barged up the rankings to eighth and ninth respectively.

The number of deals in the City fringe in particular rose by a massive 98% compared to Q3 2014, with deals at the Bower, White Collar Factory and Aldgate Tower all keeping the sector busy.

“Three years ago, there was a lot of nervousness about the quantum of space being developed on the city fringe, particularly around the Old Street roundabout,” says Shaun Simons, director at Hatton Real Estate.

“But all the buildings have now been mostly or fully let, making the fringe a real player in the London market.

“Alphabeta is a case in point. It was fringe City building. Now it’s a prime City Fringe building.”

City fringe action also played a part in Knight Frank using the quieter months to jump up the table to third place from ninth. The 275,536 sq ft letting at M&G’s Fruit and Wool Exchange to Silver Circle law firm Ashurst accounted for nearly 42% of their total.

The core markets

On closer inspection, the only markets really down in terms of take-up on last year were the City and West End.

For the City, this was more due to a bumper Q3 last year, which saw deals including M&G Investments taking 322,000 sq ft, rather than any particular drop-off in demand. Take-up was at levels far more in line with the long-term average, hovering around 987,000 sq ft.

In the West End, where take-up was down 11% on Q3 2014, it was a continuing tightness of supply driving down deal volumes, a fact of life of which agents there are already painfully aware.

According to Paul Smith, director of London offices at Colliers International, “The big problem we have going forward is a complete lack of stock.

“The bigger West End occupiers are looking two years in advance. Five years ago, a pre-let in the West End used to happen days before a building was finished. Now you are getting pre-lets of buildings under construction.”

King Digital taking 64,000 sq ft at Ampersand in Soho was one of only three deals over 30,000 sq ft in the West End, and the lack of space is even leading to the ultra-high end residential market being pipped by office development.

“The last three or four sites that one would have thought would have had residential, are getting better bids from office occupiers,” added Smith.

Very tight supply

But tight supply is not a problem exclusive to the West End, it is now common across the board, and is having more effect on take-up figures than anything else – hence the plethora of smaller deals.

“On the ground I think we are seeing a continuing shortage of small-to-medium-

sized units and an extraordinary demand for any space under 5,000 sq ft,” says Dan Bayley, head of central London office agency at BNP Paribas Real Estate.

“I suppose the other thing we are seeing is places that have not been that popular, such as Canary Wharf, having a very good year, with people getting good value deals for good quality space.”

Availability rate stands at just over 5% in the City, and less than 4% in Midtown and the West End.

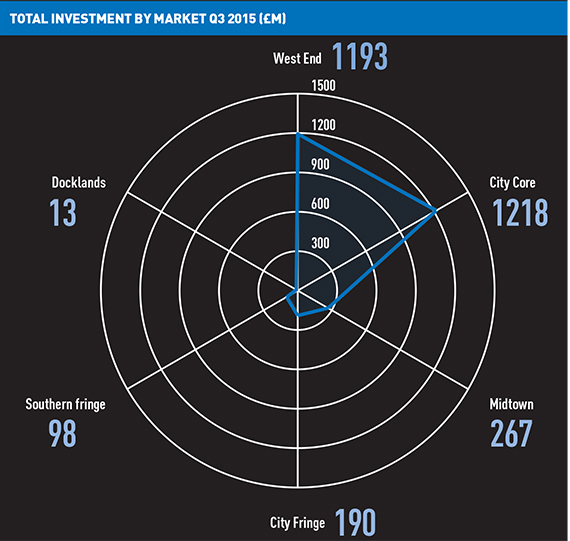

Such a small development pipeline coming forward, and much of that from refurbishments, may be bad news for take-up, but it is good news for rental growth, which is underpinning investment (see box).

According to Nick Braybrook, Knight Frank’s head of City investment: “What is really good is we are in an environment where take-up is pretty ordinary, but because of the lack of supply there is some real movement in rents. The supply could adjust in three to four years, but if the economy keeps on growing, that occupier pressure can only increase.”

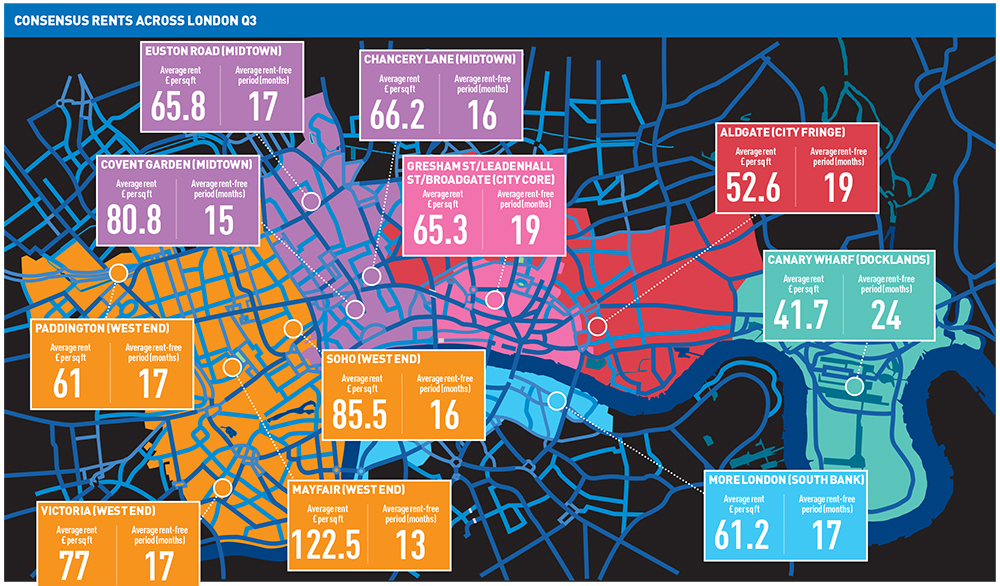

It is also particularly good news for the City, which offers comparatively good value in terms of rents compared to West End or Fringe locations (see map).

Braybrook says prime rents in the City have gone up by 11% over the past year, and Knight Frank is forecasting rises of another 20% in the next three to four years.

Relocations

Tight supply may be bad news for the core markets, but agents in the even more peripheral areas may be rubbing their hands at the thought of more back office relocations.

According to Bayley, “There are natural extensions of the central markets, and on a serious note, there is a lot of interest in places like Croydon – people no longer snigger – partly because of a lack of availability in the centre.”

On the other hand, relocations are expensive, and rents proportionately remain low in comparison to staff costs. With such a premium on recruiting and retaining the right staff, location remains extremely important.

“When faced with a limited stock, people may decide not to move,” says Pearce. “I think it’s less about price, and more about choice. You will only move if there is a compelling reason to do so.”

For the City fringe, leaps and bounds in the development of the market have attracted new tenants. Simons says: “Occupiers are not coming any more for value for money – it’s where staff want to be, clients want you to be, and companies want to be seen.”

Almost all agree that Q4 will be critical. Though traditionally the busiest quarter, as supply continues to drop, relocating the big occupiers is increasingly difficult. It may mean, at the very least, a bit more of a break over Christmas.

Rental growth underpins investment

Wobbles in the Chinese market have failed to seriously dent investment into London offices. Though headline investment was slightly down on last year, rental growth continues to be a draw.

“Both overseas and domestic buyers are focused on assets that will perform best as rent increases come through,” says Knight Frank’s Nick Braybroook. “People are very keen to get their hands on development opportunities: multi-let assets or assets with low rent passing and rent reviews coming up. If anything, it’s the longer, drier income that is harder to find a home for.

“ There is always somebody who feels that the market has an advantage for them. There’s more caution in the market, but the fundamentals on the occupational side are so strong they will win the day.”

Robb Hayes, director of London offices at Colliers International, says: “London and the West End remain the destination of choice, particularly for overseas investors.

“What we have is genuine rental growth – if you are buying on what looks like a fairly aggressive yield, you will be expecting your growth to come from rental performance.”

More stock has also been coming to the market earlier, with 15 sites on the market valued at more than £100m. And while Chinese investment may be tailing off, interest is expected from Singapore, Taiwan, Japan, and even Germany.

alex.peace@estatesgazette.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}