LOMA Q3 2020: A market down but not out

With London office take-up plummeting, agents will hope the right offering tempts occupiers back.

Rarely has the outlook for London’s office leasing market been so bleak. As the end of the year draws near, it seems all but certain that 2020 will be the poorest year on record for office take-up in the capital.

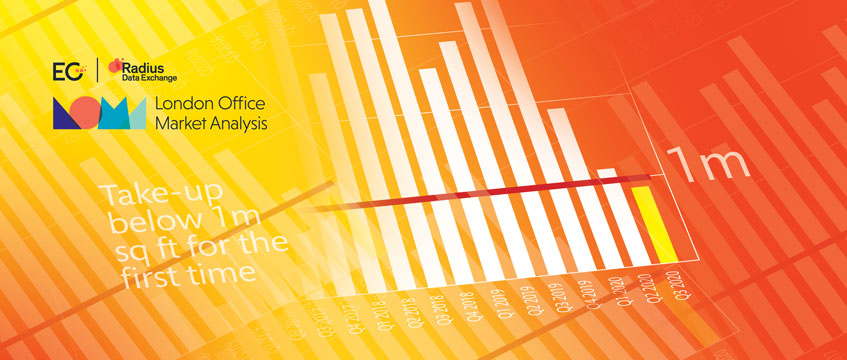

Letting volumes during the third quarter stood below 1m sq ft for the first time since EG began this series in 2002. This puts space transacted for the year so far at just above 4m sq ft – less than half of the long-term average for the opening three quarters.

With London office take-up plummeting, agents will hope the right offering tempts occupiers back.

Rarely has the outlook for London’s office leasing market been so bleak. As the end of the year draws near, it seems all but certain that 2020 will be the poorest year on record for office take-up in the capital.

Letting volumes during the third quarter stood below 1m sq ft for the first time since EG began this series in 2002. This puts space transacted for the year so far at just above 4m sq ft – less than half of the long-term average for the opening three quarters.

The causes are as clear as they are harmful. The coronavirus-driven restrictions imposed for a significant chunk of the year have made leasing transactions far tougher to get in train. Many companies are delaying decisions on leases until they have a clearer picture of how their staff will split their time between homeworking, communal headquarters and “third spaces”.

The professional sector was again front and centre in influencing take-up in central London, even in this subdued period. The sector is the third-largest occupier by footprint in London, accounting for around 13% of the city’s office floorspace, and at the start of the year accounted for a significant chunk of active requirements in the capital.

Law firm Baker McKenzie’s 153,000 sq ft deal at 280 Bishopsgate, EC2, was the only transaction to measure more than 100,000 sq ft during the third quarter. The deal meant that the market mirrored the first quarter of the year, when another significant deal for a law firm (Linklaters, also in EC2) accounted for the exact same share of quarterly leasing activity, at 16%.

Underpinned by these two transactions, professional services firms now account for more than a fifth of year-to-date take-up, making the sector the second-most active for new space let behind technology, media and telecommunications, which was boosted this quarter by Netflix taking 85,700 sq ft at the Copyright Building, W1.

The lettings to Baker McKenzie and Netflix were not enough to boost submarket letting volumes above historical figures. All six central London areas saw significant downturns on long-term averages, and were well below levels seen at this point last year.

Preletting protects rents

Grade-A rental decreases were similarly widespread. For the first time, our panel of agency bodies returned quarterly figures indicating that all 11 submarkets featured in the survey have seen rental drops – aggregated to a 1.2% decrease in grade-A rental tone across London, the sharpest quarter-on-quarter drop since this panel was formed in 2013.

This puts grade-A rents back to where they stood at the mid-point of last year, albeit with a longer typical rent-free period given at the start of the lease in comparison to 2019. Incentives increased by 6% across London compared to last quarter, according to the panel, and were up by 9% against Q3 2019.

The Radius London office rental index, based on completed deals on all grades of office space across the capital, shows a 1% year-on-year drop in rents on deals completed so far in 2020 – a much shallower fall than that which occurred the last time occupational take-up saw a sudden and dramatic tumble.

When take-up slumped at the start of 2009, the supply rate drifted outwards by 220 basis points from 7.9% to 10.1% during the first two quarters of the year, foreshadowing a full-year rental drop of 23.4% in comparison to 2008. So far this year, the availability rate has only moved by 70 basis points in nine months, even though letting volumes are less than half of the long-term average for the opening three quarters of the year.

We reported in last quarter’s analysis that healthy volumes of preletting ought to insulate the wider market from substantial rental drops in the immediate term. Prelet activity does seem to be having an impact on supply during this sedate period for new lettings, which, in turn, can slow the downward movement of aggregate rents.

But new-build completions are just one avenue of supply increase. Full and partial vacations of office units will have an impact on the availability rate during any economic recovery. That means more competition for fewer active requirements, and a rental correction that investors will keep a keen eye on in the hope of catching the bottom of the curve.

Signs from the Scalpel

Investment picked up this quarter in comparison to Q2, with just over £800m changing hands, taking year-to-date investment to £3.6bn. That marks a 41% drop year-on-year and a 63% fall on the five-year average for London office investment from January to September.

The figures were boosted by the largest individual transaction so far in 2020, when Hong Kong-based Link Asset Management made its UK debut with the £380m purchase of the Cabot, E14.

An investment fillip towards the end of the year could offer optimism going into 2021, as Google is reportedly preparing to buy Central St Giles, WC2, and activity on the newly marketed Scalpel, EC3, should offer some insight into the psyche of investors when it comes to premium stock.

If the latter building sells for anything in the region of the £820m asking price, it will be the largest individual office transaction since the £1.2bn sale-and-leaseback to Citigroup at 25 Canada Square, E14, in April 2019.

We should be cautious in concluding too much from one deal. But a capital commitment of that size for a well-located London office building in a tough time for leasing volumes and income generation in general would lift confidence that the capital’s investment credentials can endure.

Brexit looms

All eyes are now on the possibility of an economic recovery from the Covid-19 pandemic, the outcome of the UK’s negotiations with the European Union over their future relationship, and the effect that both will have on office requirements.

Occupiers are having to plot their course through a challenging set of economic circumstances. August’s GDP rebound was lower than expected and has diminished the likelihood of an optimal “V-shaped” recovery. The eventual end of the furlough scheme is likely to lead to job cuts across most business sectors, worsening an unemployment rate that has already hit a three-year high.

In addition, companies of all shapes and sizes are being asked to prepare for the end of the UK’s transition period with the EU without precise knowledge of what that will entail for different sectors.

A recent teleconference on the subject between business leaders and the prime minister was described as “perfunctory”, and reportedly offered little by way of actionable detail. The House of Lords’ European Union Select Committee has also outlined the extent to which the professional and business services sector has so far been overlooked in trade discussions, with fishing and finance taking up an outsized amount of negotiatory bandwidth.

If the interests of the professional services sector are being skated over in the dialogue between the UK and the EU, that would further inhibit the London office market’s ability to recover quickly from the arduous circumstances of 2020. Many in the market will hope that the reported mid-November deadline for trade deal negotiations brings a relatively benign set of circumstances for all business sectors.

Is homeworking here to stay?

Brexit is just one challenge for occupiers, however. Another is where work takes place in the longer term. Broad-brush surveys of business leaders suggest that remote working is here to stay in various forms. Some 59% of office-based respondents to a recent Institute of Directors survey said that their long-term intended level of office use was either slightly or significantly less than that prior to the pandemic.

This followed a poll conducted by the British Council for Offices which indicated that 62% of senior executives and 58% of entry-level workers wanted to be able to split their working week between office space and remote locations. In addition, a study from Accumulate Capital showed that 73% of UK board members, chief executives and company founders expected businesses to downsize their office space within the next 12 months.

However, some anecdotal evidence suggests that workforces in some significant business sectors are less enamoured of homeworking. More evidence will be needed before we can accurately map out the impact of workforce segmentation on different sectors.

In financial services, the loss of what one finance sociologist has called “incidental information exchange” – or random chit-chat – on in-person trading floors has led to a wholesale re-evaluation of workforce optimisation strategies at some of the world’s leading financial institutions. It has also been reported that the mood and output of Google’s remotely operating coding teams has suffered a downturn.

None of this is necessarily to say that finance and technology companies will, in unison, flood back to the office in order to satisfy traders’ and engineers’ wishes once the threat of Covid-19 is satisfactorily subdued. But it does point to a longing for communal spaces that neither workers nor their bosses appreciated before this crisis began.

And so, even after as poor a quarter and year as the London office market is experiencing, agencies, landlords and investors may find some comfort as they help London to supply the right space to keep companies working.

Reaching for the top in a struggling market

Which agencies’ roles on the quarter’s key deals let them lead the way in leasing and investment?

City Core

BH2 climbed from fourth place last quarter to take the Q3 crown in the City Core market. The agency acted on 219,000 sq ft of lettings during the three months to secure a 61.2% market share.

The top three agents all acted for the landlord on the largest deal this quarter, which saw Baker McKenzie take space at 280 Bishopsgate, EC2. Second-placed CBRE jointly acted with BH2 on the second-largest City Core deal, a 27,600 sq ft leasing to Amundi at 55 Moorgate, EC2.

BH2 gained the edge at the top of the table thanks to a pair of deals at 70 St Mary Axe, EC3 – 16,500 sq ft and 9,200 sq ft to Vattenfall Wind Power and Cubico Sustainable Investment respectively. Fourth-placed JLL acted alongside BH2 on both, and was the most active agent by deals volume in the City Core market with nine transactions completed.

City Fringe

Having come in second place in three out of the preceding four quarters, Cushman & Wakefield secured a 35.8% market share through nearly 44,000 sq ft of disposals to claim its first victory in the City Fringe submarket since Q2 2017.

Anchoring this triumph was the 38,900 sq ft letting to JA Kemp at 76-86 Turnmill Street, EC1.

Anton Page, meanwhile, secured second place with a 20.3% market share, having acted on more individual deals than any other agent in the City Fringe across the three months.

Docklands

With only two leasing deals recorded on Radius in the Docklands submarket this quarter, and CBRE acting as disposing agent on both, a rare 100% market share puts the agency in first place.

It acted as sole agent on a 22,000 sq ft deal to an undisclosed occupier at Capstan House and alongside JLL on the 12,000 sq ft deal for Fisher Investments at One Canada Square, both in E14.

Midtown

Hot on the heels of its first quarterly victory in the West End submarket earlier this year, Edward Charles & Partners tops another table, achieving a 46.9% market share in Midtown thanks to advising on more than 83,000 sq ft in new lettings.

Underpinning this success was a role alongside second-placed Savills on the largest deal in Midtown this quarter, to The Office Group at 210 Euston Road, NW1, and jointly letting 12,800 sq ft to Autodesk at 6 Agar Street, WC2, in tandem with third-placed Knight Frank.

Southern Fringe

One substantial deal was enough to enable Knight Frank to hold on to the Southern Fringe quarterly crown, which it had to share with JLL last time out. That came in the shape of an 18,300 sq ft letting to IQ-EQ at 3 More London, SE1.

Union Street Partners took second spot, having advised on more individual lettings than any other agent in this submarket. The highlight of its six deals was at 58-72 Upper Ground, SE1, where it advised on a 5,900 sq ft letting to Engage Sport Management.

West End

CBRE jumped from 12th in last quarter’s ranking to take the West End title this time around, securing a 60% market share through advising on more than 134,000 sq ft of disposals.

Having come top of the pile in Q1, Edward Charles & Partners has subsequently achieved back-to-back second-place finishes. It acted on more transactions than any other agency in the West End to secure a 16.6% market share.

Completing the top three is Levy Real Estate, which finished 11th in last quarter’s table but jumped to third on this occasion – a rise underpinned by a 10,100 sq ft deal at 55-58 Pall Mall, SW1, on which it jointly acted with sixth-placed Bluebook.

Overall leasing

Strong performances in the City Core and West End submarkets enabled CBRE to climb from fourth position in last quarter’s overall standings to top spot this time out. It advised on more deals than any other agency during the quarter, securing a 42% market share and disposing of more than 425,000 sq ft.

BH2’s involvement in the Baker McKenzie transaction helped it to climb from sixth position last quarter to second place in the overall table for Q3, while Cushman & Wakefield won a second consecutive third-place berth having advised on the same deal.

Hanover Green leapt from 16th place last quarter to finish inside the top 10 on this occasion, with a number of deals jointly disposed with CBRE at 26-28 Hammersmith Grove, W6, propelling its performance.

Overall investment

Knight Frank jumped from ninth place last quarter to claim the title for top investment advisory in Q3, acting on more than £450m worth of transactions and taking a 30% market share.

Crucial to its victory was its role advising on the £380m transaction at the Cabot, E14 – a deal on which second-placed Cushman & Wakefield also acted in order to claim a market share of 24.9%.

Putting Knight Frank over and above was the £78m deal at 7 Soho Square, W1, on which it advised the vendor, Landsec, in selling to Hines, which was represented by sixth-placed JLL.

To send feedback, e-mail graham.shone@egi.co.uk or tweet @GShoneEG or @estatesgazette

Scalpel and full moon photo © Peter MacDiarmid/Shutterstock